The Nuclear Startup Surge: Why VCs Are Betting Billions on Small Modular Reactors

For decades, the word “nuclear” was a toxic non-starter in the world of venture capital. The industry was a graveyard of ambition, defined by gargantuan government projects, forty-year construction timelines, and enough regulatory red tape to wrap around the planet twice. If you were a founder pitching an atomic startup in 2010, you were essentially laughed out of Sand Hill Road.

But as of April 2026, the narrative hasn’t just shifted—it has been completely rewritten. The grid is dying. The data centers are hungry. Nuclear is the only answer left.

We are currently witnessing a massive nuclear startup surge. The definitive catalyst? A staggering $450 million Series C round for Valar Atomics. This wasn’t just another funding announcement; it was a flare fired over the market, signaling that energy independence is no longer a soft policy goal. It is the most aggressive venture capital sector of the decade. This isn’t merely about “green” energy; it is a fundamental reimagining of how we power civilization. Silicon Valley’s “move fast and break things” ethos has finally collided with the most stable, dense energy source known to man.

The “Atomic Lego” Model: Thinking Small to Scale Big

The “why now” of this movement isn’t just about capital—it’s about a fundamental pivot in physics and manufacturing. To understand this surge, we have to look past the cooling towers of the 1970s. Traditional plants were bespoke, gargantuan feats of civil engineering. Small Modular Reactors, or SMRs, represent the industry’s “microchip” moment.

At Johny Millionaire, we call this the “Atomic Lego Model.” Instead of building a massive, one-off monument to engineering on-site, SMRs are designed as products. They have a capacity of up to 300 MW per unit—roughly one-third of a traditional reactor—and they are built in factories. They are shipped by rail, assembled on-site, and can be “stacked” to meet demand.

This modularity does more than just slash construction times. It evaporates the upfront capital risk that once terrified private equity. By treating a reactor as a manufactured good rather than a decades-long construction nightmare, startups like Valar Atomics and Oklo are turning an underdog story into a market-dominant reality. But the money isn’t just following green energy—it’s following a new kind of ravenous consumer.

How the Nuclear Startup Surge is Powering the AI Boom

The most immediate driver of this investment isn’t actually the climate crisis—it’s Artificial Intelligence. The AI expansion of the last two years has turned the United States into a landscape of energy-hungry digital fortresses. These data centers are gluttons, requiring 24/7 baseload power that the current mix of wind and solar simply cannot provide without impossibly large battery arrays.

Tech titans like Amazon, Microsoft, and Google are no longer content waiting for the aging U.S. power grid to catch up. They are moving toward a “Grid-Independent Strategy,” placing SMRs directly next to their server farms. This “direct-wire” approach ensures that even if the public grid falters under the weight of summer heatwaves or winter storms, the AI models keep training. This symbiotic relationship has transformed SMRs from a “scientific curiosity” into a “strategic necessity” for the digital age.

Read more on Johny Millionaire: Agentic AI & The Robotics Convergence: Why 2026 is the Year the “Brain” Met the “Body”

Why a16z and Founders Fund are Going “All In” on Hard Tech

The 2026 investment landscape shows a distinct preference for “hard tech”—ventures that solve physical-world problems. Both a16z and Founders Fund have led the charge, pouring billions into the nuclear sector. Their thesis is simple: the next generation of trillion-dollar companies won’t just build apps; they will build the foundational infrastructure of the 21st century.

According to the a16z American Dynamism philosophy, these VCs are betting on the collapse of the old utility model. In a world where energy demand is skyrocketing, the ability to provide localized, carbon-free, “always-on” power is the ultimate competitive advantage.

The Friction of Bureaucracy: Can Startups Really Build?

Venture capital can move at the speed of light, but nuclear energy still has to navigate the friction of a 20th-century bureaucracy. The Nuclear Regulatory Commission (NRC) has historically moved at a glacial pace, utilizing a licensing framework designed in the 1970s.

Consider the case of TerraPower. Backed by Bill Gates, the company recently broke ground on its Kemmerer Power Station in Wyoming—a massive milestone for a startup. Yet, even with heavy backing, the journey was a gauntlet of rising costs and shifting goalposts. These aren’t just technical hurdles; they are existential tests of a startup’s “burn rate.”

However, the U.S. government is finally flinching. New legislative frameworks are being fast-tracked to allow for factory-based inspections rather than on-site marathons. Startups are betting that AI-driven digital twin simulations and advanced materials, like molten salt or high-temperature gas cooling, will make these reactors “inherently safe.” This reduces the required “exclusion zones” and allows these plants to sit on the footprint of a retired coal station.

The Contrarian View: Why Some VCs are Still Hesitant

Despite the hype, it would be a mistake to assume every VC is diving in. The “liability tail” of nuclear remains a significant deterrent for traditional funds. If a software company fails, the code just stops working. If a nuclear startup fails during the operation phase, the legal and environmental cleanup could span generations. Investors who are “all in” are those who believe the technological leap to passive safety—where a reactor cools itself without human or mechanical intervention—is truly foolproof.

Read more on Johny Millionaire: Beyond the LLM: The Rise of the ‘Agentic AI’ Startup Hub in NYC Shaping the 2026 Energy Market

Key Takeaways for the Strategic Investor

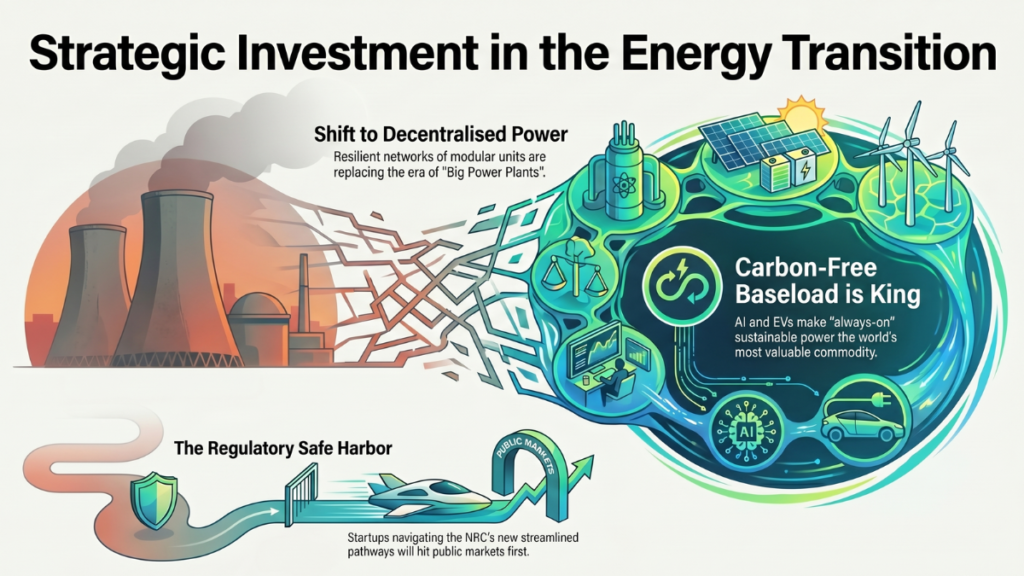

- Decentralization over Centralization: The era of the “Big Power Plant” is ending. The future is a distributed, resilient network of modular units.

- Baseload is King: As AI and EVs stress the grid, “always-on” carbon-free power is the most valuable commodity in the world.

- The Regulatory Safe Harbor: Watch for startups that successfully navigate the NRC’s new streamlined pathways; they are the ones that will hit the public markets first.

Conclusion

The nuclear startup surge of 2026 isn’t just a trend for the quarterly reports; it is the first real step toward a resilient, energy-independent America. By merging modular manufacturing with the deep pockets of “hard tech” venture capital, a new generation of founders is proving that the most traditional of industries is finally ripe for disruption. As the roar of the atom becomes the most bullish sound in the market, one thing is clear: nuclear energy is no longer a ghost of the 20th century. It is the heartbeat of the 21st.

FAQs

1. How is an SMR safer than the old plants we know?

Most SMRs use “passive safety” systems. This means they rely on natural forces like gravity and convection to cool down if something goes wrong, rather than needing pumps or electricity that could fail.

2. Why is a16z focusing on “American Dynamism” in nuclear?

Because they realize that the next trillion-dollar companies won’t just be software platforms—they will be the companies that provide the foundational energy and infrastructure that those platforms require to exist.

3. Which startups are leading the SMR race in 2026?

Currently, Valar Atomics, Oklo, and TerraPower are the frontrunners, each utilizing different cooling technologies to solve the same baseload power problem.

4. Can these reactors be built in residential areas?

Due to their small size and enhanced safety profiles, the goal is to place them on brownfield sites—like former coal plants—which are often much closer to the communities or data centers they serve.