The gold rush is over, and the dust is beginning to settle on a landscape littered with the digital remains of the “First-Wave” AI boom. Between 2023 and late 2024, venture capital poured into Silicon Valley like a pressurized firehose, inflating valuations of companies that were essentially beautiful interfaces sitting atop someone else’s brain. By April 2026, the party hasn’t just ended; the house is being sold for parts.

The carnage of 2026 didn’t happen in a vacuum; it was baked into the DNA of the 2023 frenzy. We are currently witnessing a historic AI startup collapse, with an estimated $100 billion in paper value evaporating as “wrapper” startups file for Chapter 11. What remains isn’t a thriving ecosystem of disruptors, but an “IP Graveyard” where once-vaunted patents and codebases are being scavenged by tech giants and patent trolls. But among the wreckage, three specific companies found a way to thrive—and their strategy is the exact opposite of what you’ve been told.

This isn’t just a story of business failure; it is a fundamental lesson in the psychology of hype and the brutal reality of “moat-less” competition.

The Anatomy of the 2026 AI Startup Collapse

To understand the current bloodbath, we have to revisit the “Gold Rush” phase. In the wake of GPT-4’s release, any founder with a sleek UI/UX and a background in prompt engineering could secure a $20 million Seed round. These companies promised to revolutionize everything from copywriting to legal research. However, they made a fatal strategic error: they built their houses on rented land.

As of early 2026, the trend of consolidation has turned into a rout. When the underlying model providers—OpenAI, Google, and Anthropic—integrated the “features” these startups offered directly into their core products, the startups lost their reason to exist overnight. The AI startup collapse is the natural conclusion of a market that forgot that a feature is not a company.

[Read more on Johny Millionaire: How Anthropic is Rewriting the Venture Capital Playbook]

1. The “Wrapper” Trap: Building on Rented Land

Think of a “wrapper” as a high-end paint job on a rented engine. It looks like a custom car until the landlord takes the keys back. In 2023, these were hailed as the “lean” way to build; today, they are recognized as a strategic death trap.

“If your entire business model relies on an API call to a competitor who has ten thousand times your capital, you don’t have a company—you have a temporary research project funded by VCs.” — Editorial, Johny Millionaire

The Illusion of Proprietary Tech

Most “First-Wave” failures shared a common DNA: they lacked a proprietary data moat. They were utilizing the same “brain” as their competitors. If Startup A and Startup B are both hitting the same OpenAI endpoint, the only differentiator is the color of their buttons and the aggressiveness of their marketing spend. This led to a “race to the bottom” on pricing that eventually bled everyone dry.

The “Feature vs. Product” Fallacy

Harvard Business Review has long warned about the danger of building a “feature” and calling it a “company.” We saw this with the early days of the App Store—flashlight apps were huge until Apple built a flashlight into the OS. In the AI era, this cycle moves at 10x speed. When a startup raised $50 million to do “AI-powered PDF summaries,” and then Adobe integrated that exact function into Acrobat for free, the startup’s valuation didn’t just dip—it zeroed out.

Dependency Risk and the API Pivot

Building on an API means you are subject to the whims of your provider. In 2025, several major API providers increased their “enterprise” pricing tiers while simultaneously launching competing tools. According to reports from Gartner, this “Squeeze Play” was the primary driver for 40% of the bankruptcies we see today.

2. Liquidation Logic: When Patents Become Weapons

When a tech company dies, its physical assets—the Aeron chairs and the MacBook Pros—are worth pennies on the dollar. The real value lies in the Intellectual Property (IP). But in the “IP Graveyard” of 2026, we are seeing a dark evolution in how these assets are handled.

The Rise of the AI Patent Troll

As these startups file for Chapter 11, their patent portfolios are being snatched up by Patent Assertion Entities (PAEs), commonly known as patent trolls. These entities don’t build products; they sue people who do. We are now seeing a surge in litigation where trolls use vaguely worded “AI-process patents” from failed 2024 startups to shake down profitable companies. It’s a parasitic end to what was once billed as a revolutionary movement.

The Scavenger Hunt by Big Tech

On the other side of the liquidation court are the “Hyperscalers”—Amazon, Meta, and Google. These giants are participating in “fire sales” to acquire niche talent and specific data-processing patents. This allows them to shore up their own ecosystems against antitrust regulations by claiming they are “supporting the ecosystem” while effectively absorbing the competition for cents on the dollar.

3. Founder Hubris and the Burn-Rate Culture

Success is a lousy teacher, and the easy money of 2023 was the worst professor imaginable. The AI startup collapse was accelerated by a culture that prioritized “speed to market” over “unit economics.”

The “God Complex” of 2023

Many founders believed that because they were working with “frontier technology,” the old rules of business didn’t apply. They ignored customer acquisition costs (CAC) and lifetime value (LTV) because they were too busy chasing the next valuation milestone. They forgot that AI is a tool, not a business model.

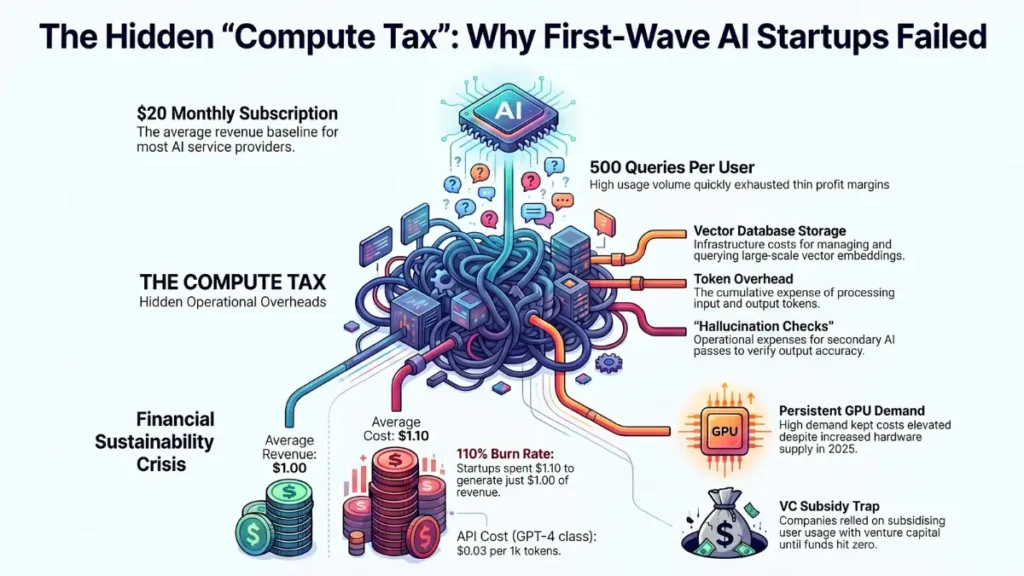

The Hidden “Compute Tax” Breakdown

The cost of running high-level AI queries is non-trivial, and it became the “silent killer” of the first wave. Let’s look at the math that broke the back of the industry:

- Average Subscription: $20/month.

- Average User Queries: 500/month.

- API Cost (GPT-4 class): $0.03 per 1k tokens.

- Hidden Costs: Vector database storage, token overhead, and “hallucination checks.”

By the time you factor in the 2025 “Nvidia-driven market shift,” where GPU demand remained high despite increased supply, many startups were spending $1.10 to generate $1.00 of revenue. They were essentially subsidizing their users’ AI usage with VC money, hoping that “eventually” the cost of compute would drop faster than their bank account would hit zero. It didn’t.

[Read more on Johny Millionaire: The Rise of the ‘Agentic AI’ Startup Hub in NYC]

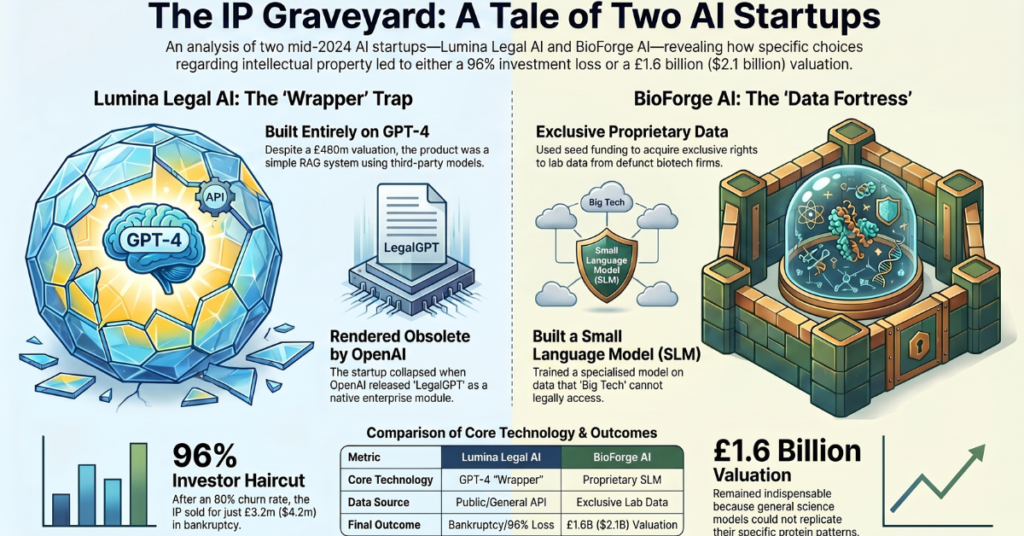

4. Comparing the Fates: A Tale of Two Startups

To truly understand the “IP Graveyard,” we must look at the specific choices that led to death versus those that led to dominance.

Representative Case A: The Fall of “Lumina Legal AI” (Failure File)

In mid-2024, Lumina raised $120 million at a $600 million valuation. Their product was a sophisticated AI interface that helped paralegals sort through discovery documents.

- The Claim: A “proprietary fine-tuned model” for lawyers.

- The Reality: It was a RAG (Retrieval-Augmented Generation) system built entirely on GPT-4.

- The Collapse: In late 2025, OpenAI released “LegalGPT” as a specialized module within their Enterprise tier.

- The Aftermath: Lumina’s churn rate hit 80% in sixty days. Their IP—mostly UI patents and a few specific data-cleaning algorithms—was sold for $4.2 million in a bankruptcy auction. The founders are now “Entrepreneurs in Residence” at a mid-tier VC firm, and the investors took a 96% haircut.

Case B: The Rise of “BioForge AI” (Success Story)

While Lumina fell, BioForge AI—founded at the same time—is currently valued at $2.1 billion. Why?

- The Strategy: Instead of using a general API, they spent their Seed round acquiring exclusive rights to proprietary lab data from defunct biotech firms.

- The Difference: They built a “Small Language Model” (SLM) trained on data that OpenAI cannot legally access.

- The Result: When Big Tech released general science models, BioForge remained indispensable because their model understood specific protein folding patterns that general models couldn’t replicate. They didn’t build a wrapper; they built a fortress.

5. The 4-Step Moat Audit for 2026 Founders

Pain is a data point. For the survivors, this $100B liquidation is the ultimate cheat sheet for the next decade. If you are building in the current climate, you must pass the Johny Millionaire Moat Audit:

- The Extraction Test: If OpenAI or Google launched your primary feature tomorrow as a free toggle, would your customers stay? If the answer is “No,” you are a feature, not a business.

- The Data Origin Test: Is your training data available on the public internet? If yes, you have no moat. You need “Dark Data”—private, proprietary, or highly regulated information.

- The Compute Margin Test: Can you be profitable today? Hoping for “future efficiency” is a gamble that $100B worth of failed companies already lost.

- The Integration Depth: Are you a destination site or a deep integration? Destination sites (where users have to log in specifically to use your AI) are dying. Success lies in being the “invisible layer” inside existing, high-friction workflows.

6. The Geopolitical Angle: AI Sovereignty and the State Factor

The AI startup collapse in the U.S. has triggered a massive geopolitical shift. As thousands of small innovators fail, the “innovation surface area” of the United States shrinks, concentrating power in the hands of a few. This has led to the rise of Sovereign AI.

The California AI Safety and Investment Pivot

In late 2025, California moved beyond mere regulation, eyeing the creation of a “Sovereign AI Infrastructure Fund.” Seeing the bankruptcy filings at the SEC pile up, state leaders realized that if private VC can’t sustain the “middle class” of tech, the state must provide subsidized compute to prevent a total monopoly.

Global Reactions

Countries like France and the UAE are now actively “headhunting” the talent from failed U.S. wrappers, offering “Sovereign AI Grants” to founders who are willing to rebuild their IP on nationalized cloud infrastructure. The U.S. “IP Graveyard” is becoming a global talent supermarket.

7. Strategic Lessons for the Next Wave

The $100B wipeout is painful, but it provides a roadmap for what actually works in the “Second Wave” of AI.

Own the Data, Not Just the Model

The only startups surviving the 2026 cull are those with “Proprietary Data Moats.” These are companies that have access to non-public, highly specific industry data. The future belongs to those who own the “Inputs,” not just the “Inference.”

Focus on Vertical Integration

Instead of being a “wrapper” for everyone, the winners are focusing on “Deep Vertical” AI. Think AI for deep-sea oil rig maintenance or specialized pediatric oncology. These niches are too small for Google to care about, but large enough to build a multi-billion dollar business.

Unit Economics First: The Death of the “Burn”

In 2026, “Profitability is the new Growth.” Investors are no longer asking about your “waitlist” or “user growth”; they are asking about your “Compute Margin.” This is the “Series A crunch of 2026″—if you can’t prove that you make more per query than you spend, your journey ends at the IP Graveyard.

[Read more on Johny Millionaire: The New Rules of Venture Capital in 2026]

8. The Psychological Toll of the “AI Hype”

We cannot ignore the human element. The AI startup collapse has left thousands of highly talented engineers in a state of professional crisis. For years, the “Millionaire Mindset” was equated with “Growth at all costs.” In 2026, the elite mindset has shifted toward Resilience and Sustainability.

The founders who survived are those who had the discipline to say “no” to easy money and “yes” to hard problems. They didn’t chase the hype; they chased the value.

The Millionaire Post-Mortem Checklist

- Audit Your Dependencies: Map out every third-party API your business relies on. Create a “kill switch” plan for each.

- Evaluate Your IP: Are you protecting a UI, or are you protecting an algorithm? UI patents are currently worthless in the IP Graveyard.

- Check Your Margins: If your compute costs are higher than 20% of your revenue, you are in the danger zone for the 2026 market.

- Deepen the Moat: Invest in “Dark Data” acquisition immediately.

Frequently Asked Questions (FAQs)

Q: What exactly is an “AI wrapper”?

A: An AI wrapper is a software application that provides a custom user interface but relies on a third-party Large Language Model (like GPT-4) via an API to perform its core functions. It’s the digital equivalent of putting a fancy cover on a borrowed book.

Q: Is the AI bubble bursting in 2026?

A: It’s not a “burst” as much as a “re-alignment.” While “wrapper” startups are collapsing, infrastructure, hardware (chips), and deep-vertical AI continue to see massive, sustainable growth.

Q: How can a new founder avoid the “Wrapper Trap”?

A: By focusing on “Sovereign AI”—building models or workflows that utilize proprietary data and can function independently of a single massive API provider.

Q: Who is profiting from the IP Graveyard?

A: Patent trolls and “Hyperscalers” (Big Tech). They are buying up the wreckage of 2024’s unicorns for pennies, either to sue others or to integrate the tech into their monopolies.

Conclusion: The Phoenix from the Ashes

The $100 billion “IP Graveyard” is a somber reminder that in the world of high-stakes technology, novelty is not a substitute for a business moat. The “First-Wave” startups were the scouts—they went out, found the territory, and in many cases, died there.

But their failure is the fertilizer for the next era of innovation. The “Second-Wave” startups arriving in mid-2026 are leaner, meaner, and far more strategic. They aren’t interested in being “the AI for X”; they are interested in solving “Problem Y” so effectively that the AI becomes invisible.As we look across the landscape of collapsed unicorns and liquidated patents, the lesson is clear: Don’t build a better wrapper. Build a better foundation. The future of wealth isn’t in the prompt; it’s in the data, the discipline, and the durability of the model.

[…] Read more on Johny Millionaire: The IP Graveyard: Lessons from the $100B Collapse of “First-Wave” AI Startups […]